Metrics that matter: 3 practical observations on valuation

As part of the Metrics That Matter series, we’ve written about three analyses to track the path to profitability and two metrics to calibrate retention and expansion. These metrics serve as both outputs and inputs. They are outputs from the activities of people at companies working hard to create compelling products, distribute them to customers, and drive the business forward. They are also inputs to valuation, a topic especially pertinent in today’s market.

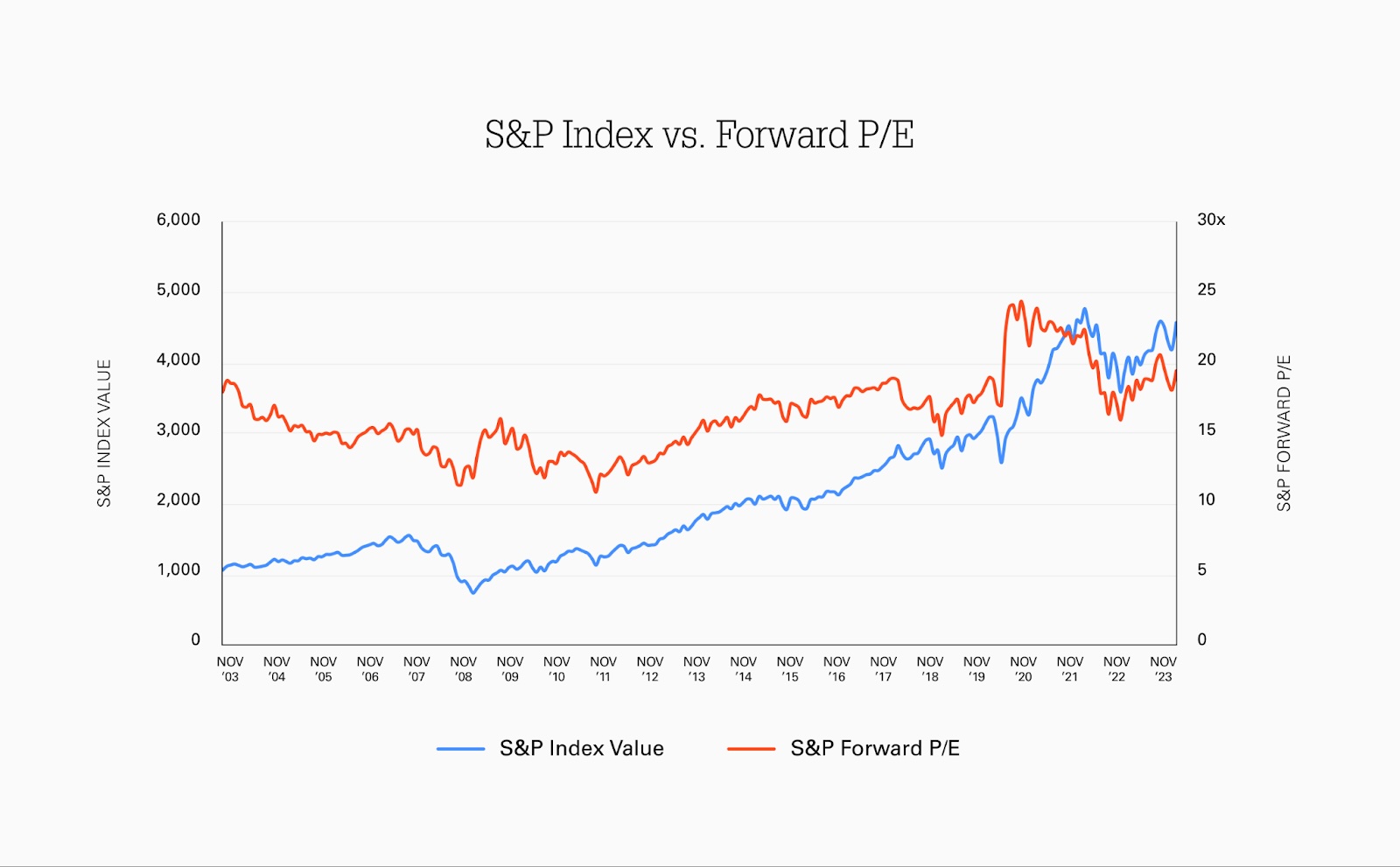

We are fast approaching the two-year anniversary of an all-time high for the S&P in January 2022. After a tumultuous 2022 and 2023, the S&P rallied in November and is now re-approaching the high, with valuation multiples also coming back due in part to the rise of the “Magnificent Seven” (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla), as well as investor optimism around the potential for interest rate cuts.

Image Credits: Index Ventures

Given the whiplash, founders, operators, investors, and analysts alike are left wondering how to think through valuation in anticipation of 2024.

Over the years, there has been some widely praised and well-researched classic literature on valuation, but these guides can be hundreds (or thousands) of pages, often leaving readers overwhelmed.

With that in mind, here are three practical observations on valuation for founders:

- Interest rates govern public and private company valuations.

- Focus on durable, high-quality revenue growth.

- Valuation is driven by sentiment in the short-term and fundamentals in the long-term.

Interest rates govern public and private company valuations

High-performance coaches recommend that clients “control the controllables.” Unfortunately, interest rates are not one of those controllables.

Founders, operators, investors, and analysts alike are left wondering how to think through valuation in anticipation of 2024.

The Federal Reserve sets monetary policy as a way to achieve low and stable inflation in the price of goods and services. When the Fed increases rates, it becomes more attractive for individuals to save rather than spend. The same is true for investors. If it’s more advantageous to invest in risk-free government bonds, investors expect higher returns to invest in risk-bearing stocks.

When it comes to valuation, the public market typically talks over time about multiples of earnings, meaning net income or profit. For example, a price-to-earnings (P/E) multiple of 20 means that a company with $1 of earnings per share is valued at $20. A 20x P/E multiple implies a 5% earnings yield (1/20). If a company does not yet have earnings, analysts will refer to other proxies for earnings such as revenues, gross profit, or EBITDA.

When interest rates increase, multiples decrease because investors demand a higher yield to invest in equities rather than bonds. We can see this by plotting the 10Y Treasury bill rate against the S&P forward P/E multiple.